In many cases, the product won’t be sellable at splitoff, because the product isn’t finished yet. In the following year, the market value of the green widget declines to $115. The cost is still $50, and the cost to prepare it for sale is $20, so the net realizable value is $45 ($115 market value – $50 cost – $20 completion cost). Since the net realizable value of $45 is lower than the cost of $50, ABC should record a loss of $5 on the inventory item, thereby reducing its recorded cost to $45. The cost to prepare the widget for sale is $20, so the net realizable value is $60 ($130 market value – $50 cost – $20 completion cost). Since the cost of $50 is lower than the net realizable value of $60, the company continues to record the inventory item at its $50 cost.

Step-by-Step Guide to Calculating NRV

Net realizable value (NRV) in accounting is the estimated selling price of an asset in the ordinary course of business, minus any costs to complete and sell the asset. NRV provides a conservative estimate of an asset’s value, ensuring financial statements reflect realistic asset valuations. Net realizable value is an essential tool in accounting, ensuring that asset values are reported accurately and conservatively.

Scope of onerous contracts requirements is broader under IFRS Standards than US GAAP

In terms of accounting work, staying current with these economic shifts is paramount for accounting processes, particularly when applying NRV analysis in financial reporting and inventory management. Businesses also need to consider industry-specific factors like technological advancements, regulatory changes, or international trade agreements, all of which can shift market conditions and, in turn, impact NRV. By leveraging tools like a record to report suite, companies can more efficiently keep a pulse on these economic indicators, allowing for real-time adjustments to accounting reports and better anticipation of shifts in NRV.

- A new assessment of net realizable value should be made in each subsequent period.

- This aspect of accounting is pivotal in presenting a transparent view of a company’s financial health, which stakeholders rely on for making informed decisions.

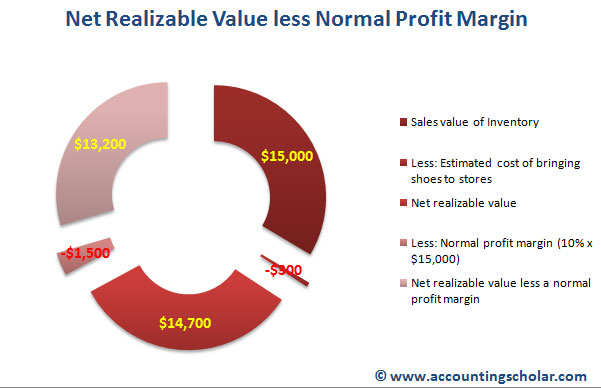

- In brief, LCM allowed accountants to measure inventories at the lower of historical cost or market value, where market value could mean replacement cost, net realizable value (NRV), or NRV less a normal profit margin.

- Businesses also need to consider industry-specific factors like technological advancements, regulatory changes, or international trade agreements, all of which can shift market conditions and, in turn, impact NRV.

- The percentage of gross profit margin is revised, as necessary, to reflect markdowns of the selling price of inventory.

What Is a Suspense Account: Definition, Types and Examples

Net realizable value calculations are a simple yet incredibly effective way to determine your potential losses when selling inventory or offering credit to customers and clients. While this could prompt changes within your billing processes, it also means that you can make more informed decisions on who to extend credit to moving forward or on how you’d like to manage your future receivables. As evidenced above, net realizable value is a vital tool for making informed decisions about the performance of your accounts receivables and the value of assets and your inventory. Net realizable value (NRV) is a method used to determine the actual value of an asset when sold, after deducting any costs involved in the sale.

This is often reduced by product returns or other items that may reduce gross revenue. It can also simply be done for just a single item rather than a group of units. In regards to accounts receivable, this is equal to the gross amount to be collected without considering an allowance for doubtful accounts.

KPMG Executive Education

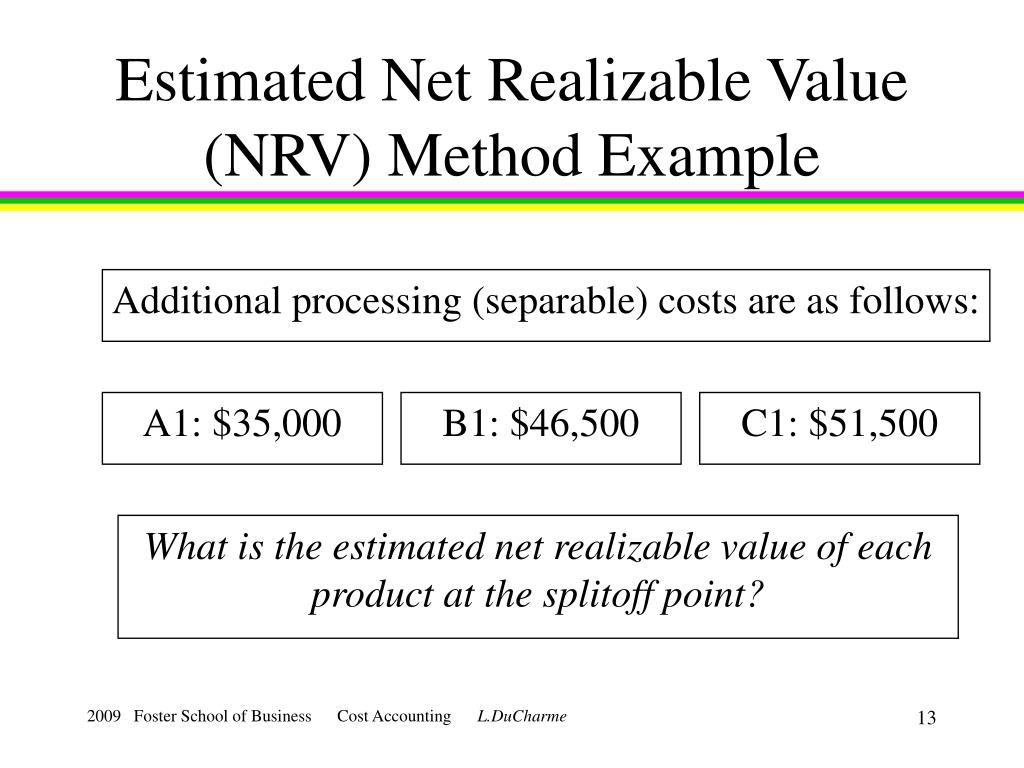

The net realizable value method allocates joint costs on the basis of the final sales value less separable costs. Final sales value is simply the price tag — the price paid by the customer. That price is paid after all production costs, whether they are joint costs or separable costs incurred after splitoff. When doing the NRV calculations for accounts receivable, the allowance for doubtful accounts or bad debts takes the place of total selling costs.

HighRadius Autonomous Accounting Application consists of End-to-end Financial Close Automation, AI-powered Anomaly Detection and Account Reconciliation, and Connected Workspaces. Delivered as SaaS, our solutions seamlessly integrate bi-directionally with multiple systems including ERPs, HR, CRM, Payroll, and banks. Our solution has the ability to prepare and post journal entries, which will be automatically posted into the ERP, automating 70% of your account reconciliation process. It allows users to extract and ingest data automatically, and use formulas on the data to process and transform it.

This helps businesses determine the net amount they can expect to receive from selling an asset after accounting for any additional costs involved in the sale. In a real-world scenario, let’s unpack how a company might compute the NRV for its accounts receivable. TechGadgets Inc., has an outstanding AR balance that needs careful examination to gauge its creditworthiness. With an anticipated invoice for $5,000 from a customer, TechGadgets Inc. must factor in a collection cost of $200. Additionally, considering customer liquidity problems or poor economic conditions, the company prudently anticipates that $300 may not be recoverable due to potential bad debt, aligning with the principle of conservatism.

When it comes to business longevity, consistent cash flow, effective inventory management, and proper financial planning are critical. This is because it helps you to determine the value of your accounts receivables and inventory value.This article will help business owners or those in charge of managerial accounting tasks better understand their net realizable value. Knowing your net realizable value is about more than being able to determine the expected selling price of an asset, product, or service. For example, you should also endevor to set up comprehensive payment terms, use automation, and conduct regular credit checks. Chaser can also be used to help you determine the best net realizable value method for your business.

No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation. Like IAS 2, transport costs necessary to bring purchased inventory to its present location or condition form part of the cost of inventory. Unlike IAS 2, US GAAP does not contain specific guidance on storage and holding costs, which may give rise to differences from IFRS Standards in practice.

It has a wooden table in its inventory, and the expected selling price is $1,000. To sell this table, the company needs to spend $50 on finishing touches, $100 on packaging, and $50 on shipping. Net Realizable Value is the value at which the asset can be sold in the market by the company after subtracting the estimated cost which the company could incur for selling the said asset in the market. It is one of the essential measures accounts payable job description for the valuation of the ending inventory or receivables of the company. It’s essential to be thorough in this accounting, considering every expense that relates directly to the completion and selling of the asset, including the respective closing costs that reflect the concluding stages of the sale transaction. This could range from packaging to transportation, and may also encompass commissions and fees tied to the sale.